The Ins and Outs of Lithium Batteries | With a Bright Industry Future, CATL Surpasses PetroChina

2021-04-09 16:33:24

Contemporary Amperex Technology Co. Limited (CATL), the lithium battery giant and ChiNext “bellwether,” went from a nonentity to the world’s largest EV battery company in under 7 years, and its market capitalization has even surpassed energy industry behemoth PetroChina.

A lithium battery (Li-ion battery) is a type of battery that has lithium metal or lithium alloy as an anode and uses non-aqueous electrolyte solvents. The development of the electronics sector has seen lithium batteries dominate the battery market for consumer electronics such as mobile phones and notebook computers. Thanks to continuous growth in new energy vehicles (NEV), the lithium battery industry has ushered in a new round of development opportunities.

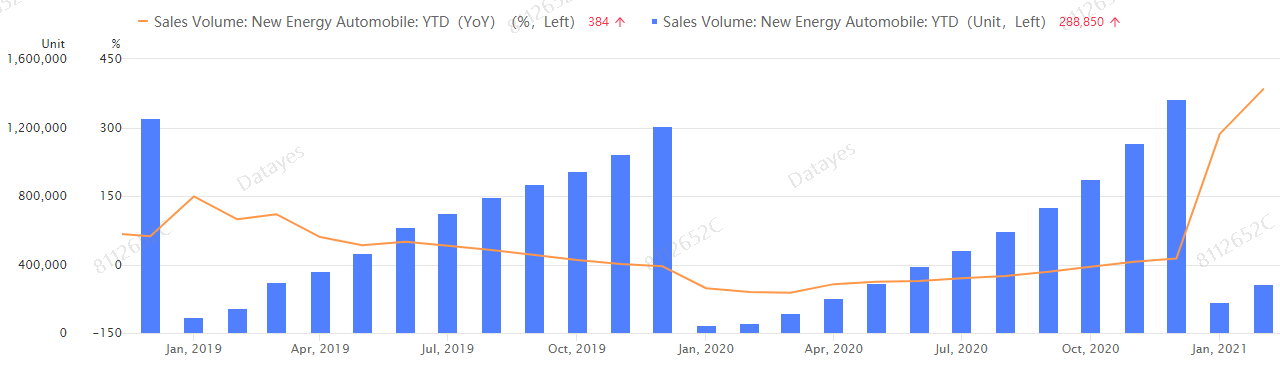

CATL has capitalized on this general trend and is now a major supplier in the NEV industry. The total number of NEVs sold in China stood at 1.206 million in 2019, and rose to 1.367 million in 2020, a year-on-year increase of 10.9%. As NEVs become increasingly popular in the future, the lithium battery industry will continue to grow rapidly.

The battery required to power an NEV accounts for about 30-40% of the cost of manufacturing a vehicle. Japan’s Panasonic and South Korea’s LG and Samsung have long dominated the global power battery industry. However, starting in 2017, CATL has emerged to take the crown in the world power battery market in terms of sales volume for three consecutive years.

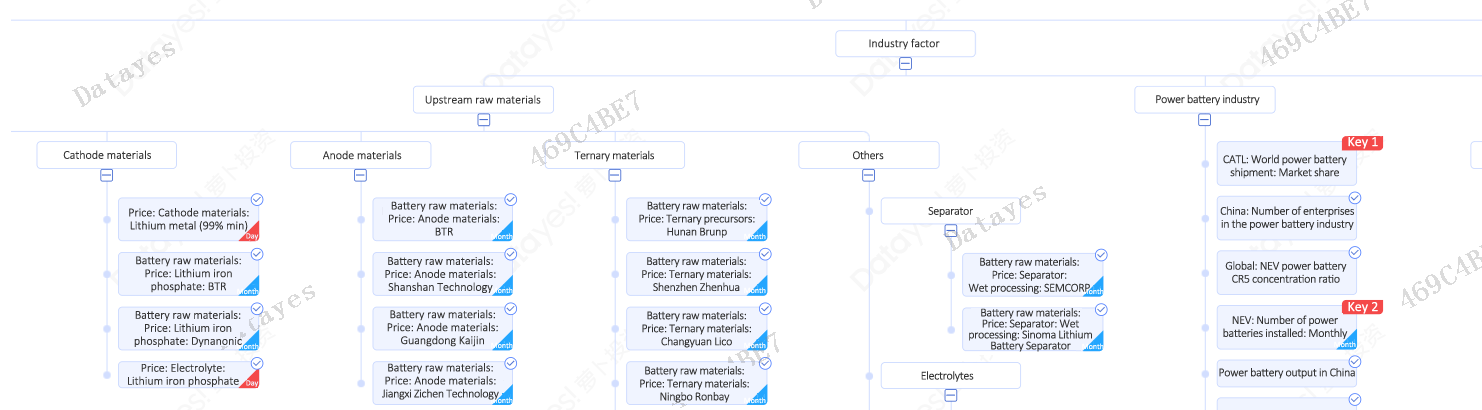

One can see from CATL’s research framework that the company’s upstream raw materials include cathode and anode materials, ternary materials, electrolytes, and separators.

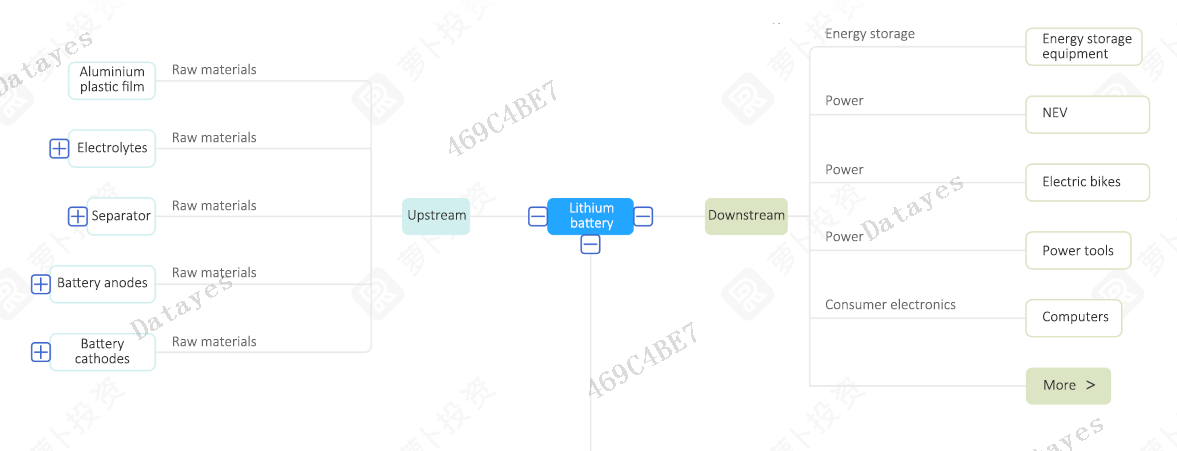

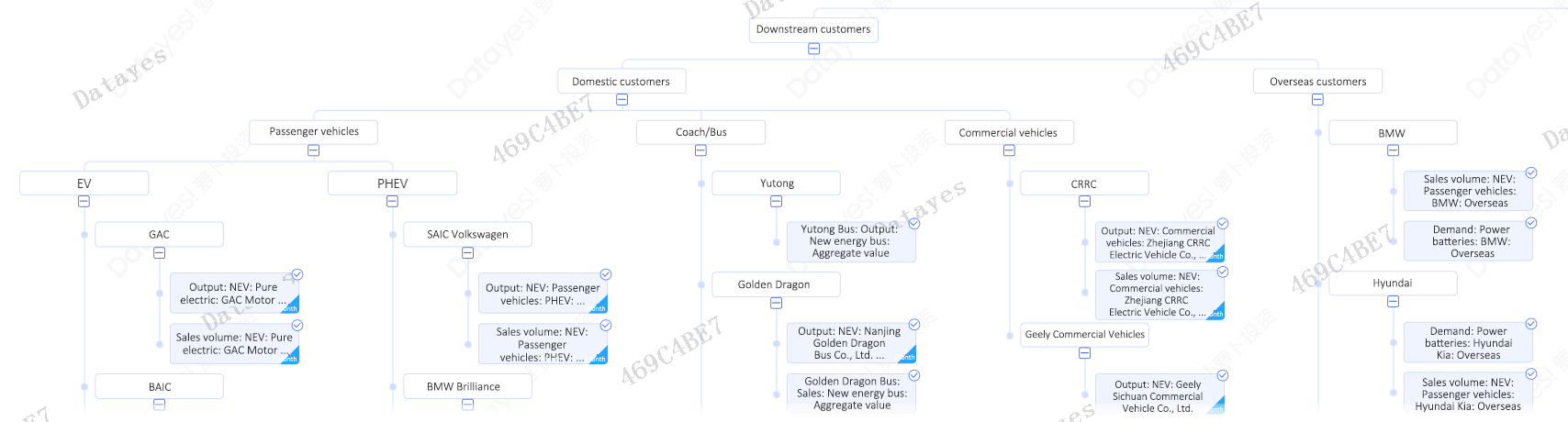

According to the Datayes knowledge graph – in the up- and downstream industry chain, there are four core upstream components in a lithium battery, namely, cathodes, anodes, separator and electrolytes. Based on different application scenarios, there are three major downstream sectors, such as wind power storage, base station backup energy storage and other energy storage sectors.

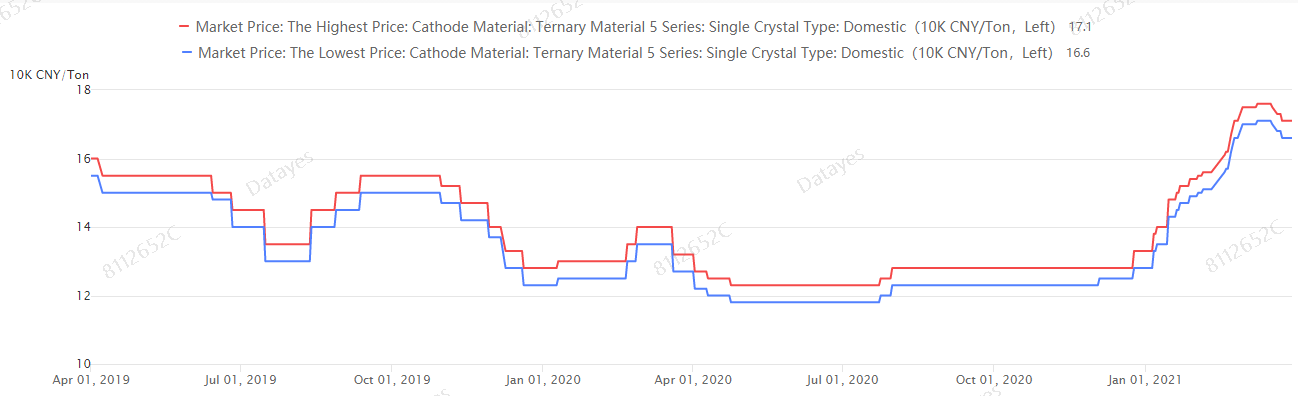

Cathode materials, a critical component in a lithium battery, generally account for 30%-40% of the total cost of a battery, and is a factor that has a direct impact on lithium battery performance indicators such as energy density and safety. Currently, commercialized cathode materials in the market include: lithium cobalt oxide, lithium manganese oxide, lithium iron phosphate and ternary materials.

Lithium battery anode materials are primarily comprised of carbon and non-carbon materials, which account for about 10% of total cost of a lithium battery.

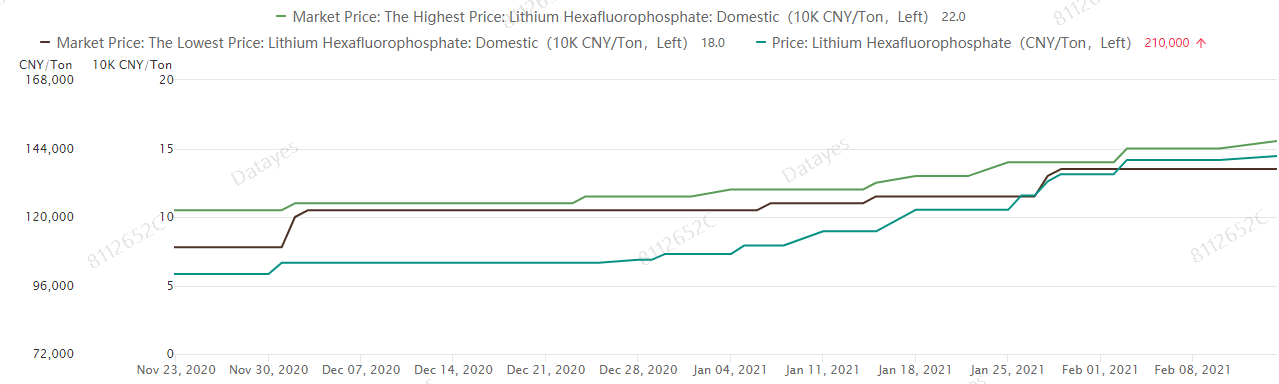

In terms of carbon materials, natural and artificial graphite are most commonly used. Electrolytes are one of the four major materials used in a lithium battery, and generally comprise about 7% of the total cost of a battery. Electrolytes are generally comprised of solutes, solvents and additives, of which, electrolyte solutes account for the largest share of the cost. That is, approximately 60% of the cost of electrolytes. Therefore, the price of solutes has a significant impact on the price of electrolytes. Currently, lithium hexafluorophosphate is the most widely used solute. As a result, electrolyte prices fluctuate in tandem with that of lithium hexafluorophosphate.

The separator, a key lithium component, is used to ensure rapid ionic transport, and separate contact between anodes and cathodes.

We can integrate this upstream raw material data into CATL’s research framework, and alert investors when raw material prices exhibit unusual movements.

CATL has maintained its gross margin at about 40%. The industry’s gross margin has, on the whole, declined over the last two years, but CATL’s has fallen less than the average level. This indicates excellent cost control ability.

Presently, many of the company’s projects under construction have yet to achieve capacity. CATL has invested RMB10 billion to lay out and plan a 45 Gwh lithium battery NEV plant at Cheliwan, Ningde, which is expected to produce at capacity by the end of 2021. It also plans to invest another RMB19.7 billion to expand its capacity to a total of 52 Gwh. As production capacity increases, its market share is expected to further rise.

CATL is also actively teaming up with downstream auto manufacturers by establishing joint ventures in order to lock in demand. BAIC, SAIC, Dongfeng, Changan Auto and NIO have in-depth collaborations with CATL.

We can similarly integrate downstream demand figures into the research framework, and use this relatively high-frequency data to promptly adjust the results expectations of the company. Investors can also list such data on their dashboards and monitor it on their own. Changes to such figures will be transmitted to the earnings forecasts of the company, and such forecasts will be automatically updated.

Datayes has built up a massive database, and dissects the principal business activities of each stock from a fundamental investment research perspective. It quantifies the factors through a “macro-industry-stock” top-down approach, and builds the corresponding data into the framework, thereby constructing a research framework for each stock.

Thanks to big data and knowledge graphs, machine learning and other technologies, investors now have an automated research framework, and just like CATL, can master changes in the performance of listed companies.

Customer Hotline: 400-082-0386

E-mail: info@datayes.com

Address:9th Floor, Wanxiang Building, No. 99 Lujiazui West Road,

Pudong New Area, Shanghai 200120 PRC

Follow Dateyes!

https://www.linkedin.com/company/datayes

Intelligent Investment Research

Fund Investment Advisor

Intelligent FOF

Portfolio Analysis and Risk Management

Quantitative Investment

Customer Hotline:400-082-0386

E-mail:info@datayes.com

Address:9th Floor, Wanxiang Building, No. 99 Lujiazui West Road,

Pudong New Area, Shanghai 200120 PRC